Gold's 2025 Surge: Understanding the Drivers and Outlook for 2026

We are predicting a rise in gold prices up to $5300/toz due to an increase in private sector investment into the gold market.

Private sector investors hedge into gold primarily as a strategic diversifier and protection against persistent macro and policy uncertainties. Amid elevated geopolitical risks, fiscal sustainability concerns in advanced economies, potential currency debasement from high debt levels, and lingering inflation pressures, gold serves as a non-yielding asset with low correlation to traditional stocks and bonds, offering downside protection during market drawdowns or periods of volatility.

Key Catalysts Fueling Gold's Upward Momentum

Recent trends show private-sector demand broadening beyond central bank buying, with inflows into gold ETFs, physical bars/coins, and derivatives (like call options) reflecting "sticky" hedges against global policy risks—such as sanctions exposure, monetary fragmentation, or unexpected shifts in interest rates.

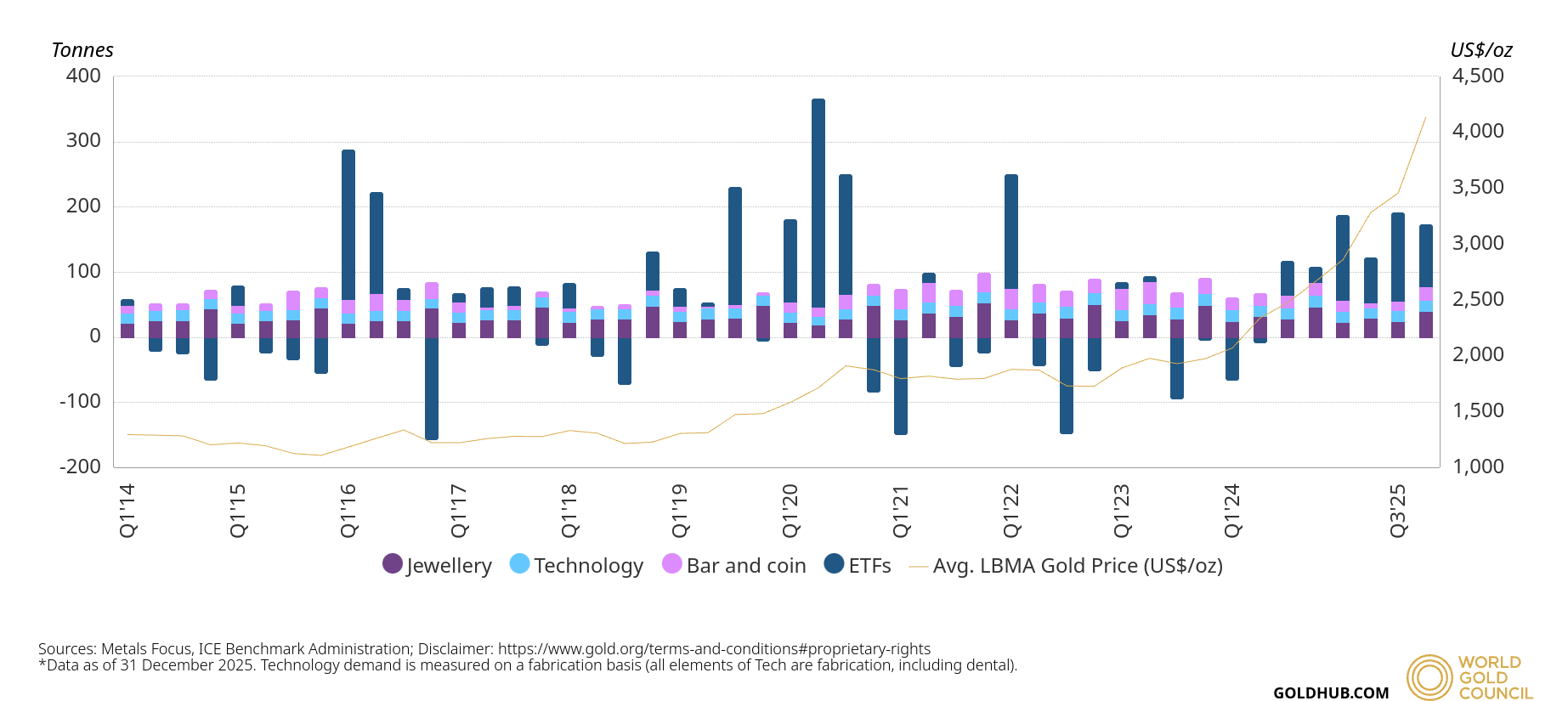

Exhibit 1: Gold ETFs dominated US gold demand in every quarter of 2025

The surging gold price, which reached 53 new all-time highs in 2025, created a self-reinforcing cycle of demand: as prices climbed, investment in gold ETFs increased in tandem with the rising underlying value of the metal. Consequently, gold ETFs emerged as a dominant force in the market, contributing approximately two-thirds of both quarterly and full-year demand.

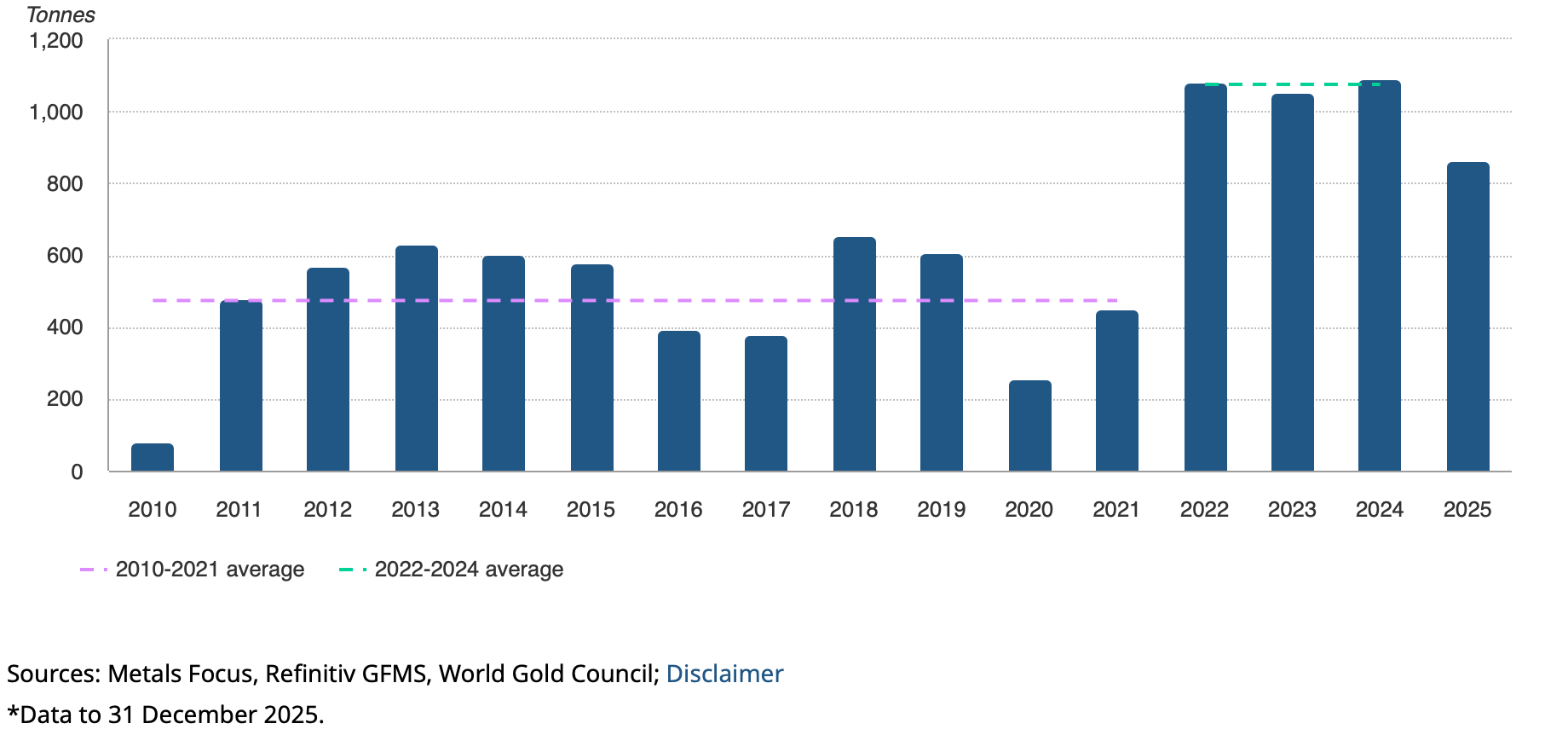

The strong momentum in central bank gold purchases, which intensified after Russia's reserves were frozen in February 2022, played a key role in supporting gold's price gains of 15% in 2023 and 26% in 2024. This official-sector demand became even more pronounced in 2025, fueling a dramatic 67% rally and pushing prices to new highs, with the spot gold price currently around $4,980 year-to-date. The acceleration stemmed from central banks increasingly competing with private investors for a constrained supply of physical bullion.

This sustained official buying continues to underpin the market's structural strength, even as private-sector ETF inflows have also surged in response to the rising price environment.

Exhibit 2: Central bank gold demand

Twenty-two central banks reported adding roughly one tonne or more to their gold reserves over the course of 2025, with just seven institutions accounting for the majority of the year's net purchases. The remaining buying activity came from a broad group of smaller, consistent acquirers, creating a diversified base of official-sector support for the market.

This pattern of widespread yet concentrated demand from central banks aligns with the broader momentum seen in private investment flows, where ETF inflows have also accelerated amid the price rally.

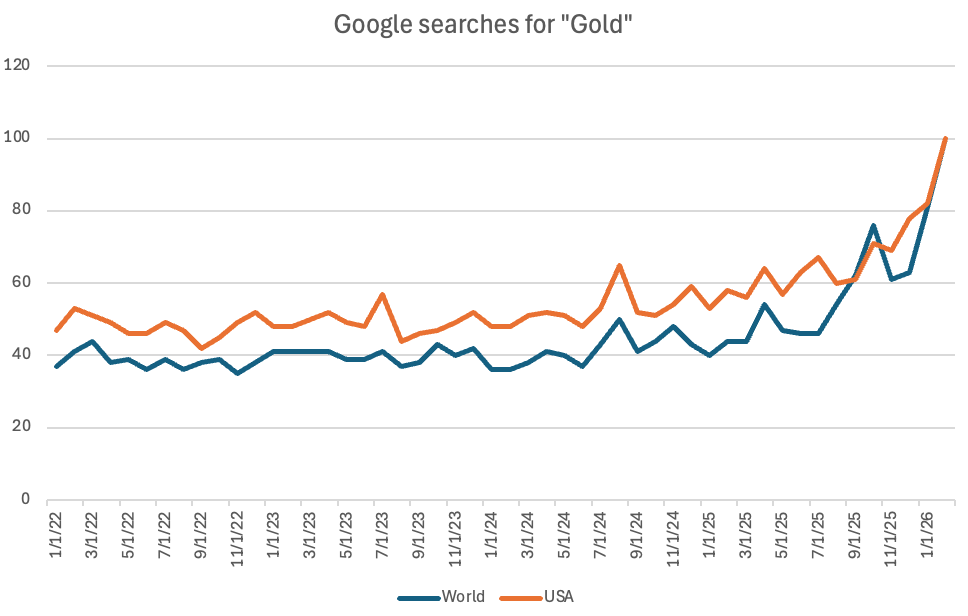

Additionally individuals buying gold has increased with high net worth families looking for ways to store gold as a hedge against inflation.

Exhibit 3: Google trends for “Gold”

Source: Google trends

In 2025, a notable portion of central bank gold accumulation continued to occur without immediate public disclosure. The persistent difference between Metals Focus' comprehensive estimates and officially reported figures points to significant unreported activity, accounting for approximately 57% of the year's total purchases. This pattern suggests that certain official institutions are steadily building their reserves discreetly—a trend that has been evident across recent years and reflects strategic timing or policy preferences among some buyers.

This element of opaque official demand adds another layer of structural support to the gold market, complementing the visible private-sector inflows and the self-reinforcing price cycle driven by ETF investment.

The Enduring Impact of Macro Policy Hedging on Gold Prices

It is our assumption that the driver behind golds price rise is individuals, private institutions and central banks hedging against potential changes in global macro policy and that these hedges will remain in place through 2026.

This stands in contrast to similar situations such as in early 2020 (gold rose ~25–30% from January to August peaks around $2,000/oz) as a hedge against pandemic-induced lockdowns, economic shutdowns, and massive uncertainty. The initial flight-to-safety was sharp, but as central banks flooded markets with liquidity and vaccines brought optimism, gold corrected notably in late 2020–early 2021 (down ~15–20% from highs).

These perceived macro policy risks—such as concerns over long-term fiscal sustainability—appear to have taken on a more durable character among investors. Accordingly, we anticipate that hedging activity directed at these global macro policy uncertainties will remain relatively steady through 2026, as many of these underlying issues (e.g., structural debt dynamics or policy fragmentation) are unlikely to fully resolve within the year.

When would we revise our position

Gold rallies tend to reverse primarily when overall demand begins to weaken, which typically occurs due to one or more of the following developments: (1) a meaningful easing of geopolitical tensions that reduces the need for central banks to diversify reserves into gold; (2) a reduction in perceived macro policy risks (such as long-term fiscal sustainability concerns) that lessens private investors' motivation to hedge; or (3) a shift in Federal Reserve policy from rate-cutting (which supports ETF inflows by lowering opportunity costs) to rate-hiking.

On the central bank side, a sustained decline in central bank demand toward or below pre-2022 levels (around 16 tonnes per month) would serve as a significant warning signal. Central bank gold demand has historically moved in extended cycles: net purchases often accelerate when the perceived neutrality or safety of traditional reserve assets weakens, as seen in the 1970s or following the 2022 freezing of Russian reserves. Conversely, once hedging needs subside, urgency to accumulate gold diminishes.

From the private-sector perspective, Federal Reserve rate hikes could dampen gold demand through two channels: the classic opportunity-cost effect (higher yields make non-yielding assets less attractive) and reduced investor anxiety about central bank independence or policy credibility.

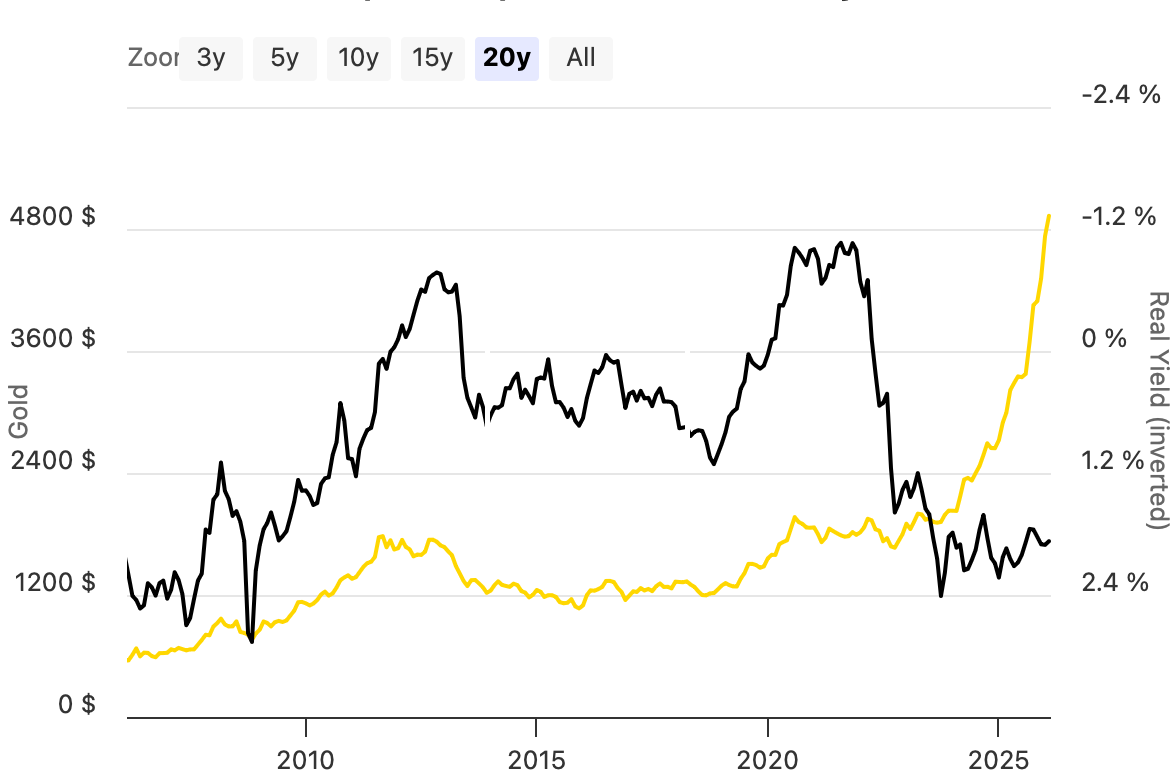

Gold Prices and Real Yields

Gold's relationship with bond yields is most reliably characterized as an inverse correlation with real yields (nominal Treasury yields adjusted for expected inflation, such as 10-year TIPS yields) rather than nominal yields alone. When real yields decline, the opportunity cost of holding non-yielding gold falls, making it more appealing relative to interest-bearing assets like bonds. Historical data shows strong negative correlations (frequently in the -0.6 to -0.8 range over multi-year periods) during eras of low or negative real rates, such as post-2008 quantitative easing or 2019–2021.

However, this link is not fixed and has shown notable weakening or decoupling in recent years (particularly since 2022–2023 and into 2026). Gold has at times risen or held firm even as real yields increased, supported by structural drivers including persistent central bank accumulation, geopolitical uncertainty, fiscal/debt concerns, and private-sector diversification flows that outweigh traditional yield sensitivity. Nominal bond yields exhibit an even less consistent inverse relationship with gold, as both can occasionally move in the same direction during inflationary or risk-off environments where traditional macro correlations break down.

Exhibit 4: Gold (inverted) Real 10 Year Treasury Yield

In summary, our outlook for gold remains constructive, with prices potentially climbing to $5,300 per ounce amid sustained demand from private investors, central banks, and high-net-worth individuals hedging against persistent uncertainties. While structural supports like diversification needs and official buying provide a strong foundation, vigilance is essential for potential reversals tied to easing risks or Fed policy shifts.